1 min read

Score a Touchdown with FranFund

When it comes to getting funded with a Small Business Administration (SBA) loan, you must be confident in your game plan. You cannot win a game...

Federal Reserve interest rates have been a hot topic in the news lately. With the Fed reducing rates last week, this is a great time to understand what Fed interest rates are and how they affect franchise financing.

What are Fed Interest Rates?

The Federal Reserve – or “the Fed” – is our country’s central bank. The Fed was created by Congress in 1913 to address the problem of bank runs. Today, the Fed manages our money supply, helps maintain fiscal stability, and guides our economic positioning.

The federal funds rate is what banks and credit unions charge each other to lend Federal Reserve funds. Financial institutions with excess balances in their accounts lend those balances to institutions in need of more funds. In broader terms, it’s a tool the Fed uses to help manage our country’s economic growth.

One of the most significant rates influenced by the federal funds rate is the prime rate, which is the rate banks charge their customers. Small Business Administration (SBA) interest rates are based on the prime rate (currently 4.75%) plus the bank’s rate, which can vary depending on the bank, SBA loan program, and strength of the borrower/franchise.

What Does this Mean Outside of Banking?

When the Fed lowers interest rates, this stimulates economic growth. Lower financing costs encourage borrowing and lending in the private sector; when rates go down, money gets “looser” because borrowing becomes less expensive. This affects all areas of the economy.

What Does this Mean for Franchise Financing?

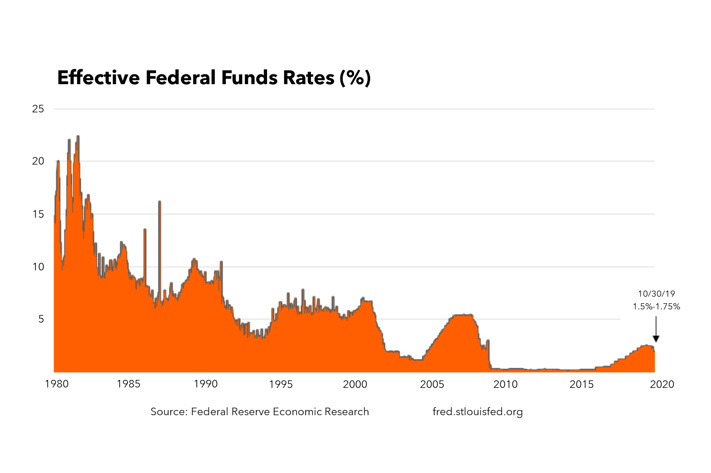

Historically, single-digit interest rates are not the status quo. As you can see in the graph below, Rates were >20% as recently as the '80s.

More recently, interest rates were dropped below 5% in response to the 2000-2002 recession. They then crept back to 5% and were dropped again in response to the Great Recession. Interest rates were finally back on the rise last year, but global economic uncertainty has led the Fed to reduce them again.

Although this may appear ominous, it’s great news for new franchisees, as the cost of borrowing money is now lower. Qualified small business owners applying for SBA loans or traditional bank loans will be able to secure funding at much more attractive rates. If you’re already a franchisee, this could be a great time to expand. Our economy is strong, and capital is historically cheap. And should the most bearish scenario occur, many franchised businesses are well-equipped to thrive in downturns.

There are many factors to consider when starting or expanding your business, and the cost of borrowing should always be one of them.

1 min read

When it comes to getting funded with a Small Business Administration (SBA) loan, you must be confident in your game plan. You cannot win a game...

1 min read

The entry costs to start a franchising business vary based on brand, location, industry (quick service restaurant, travel, beauty, etc.), and level...

1 min read

It has been more than seven months since the coronavirus pandemic began. Although the business world has been upended, there are signs of improvement...