A credit score is essentially a grade for your creditworthiness. It gives lenders an idea of how quick and reliable you are when paying back debts. Along with equity, collateral, and burn rate, credit score is one of the main qualifiers for business loans.

While there are various credit scoring models, the five factors that affect your score are almost always the same:

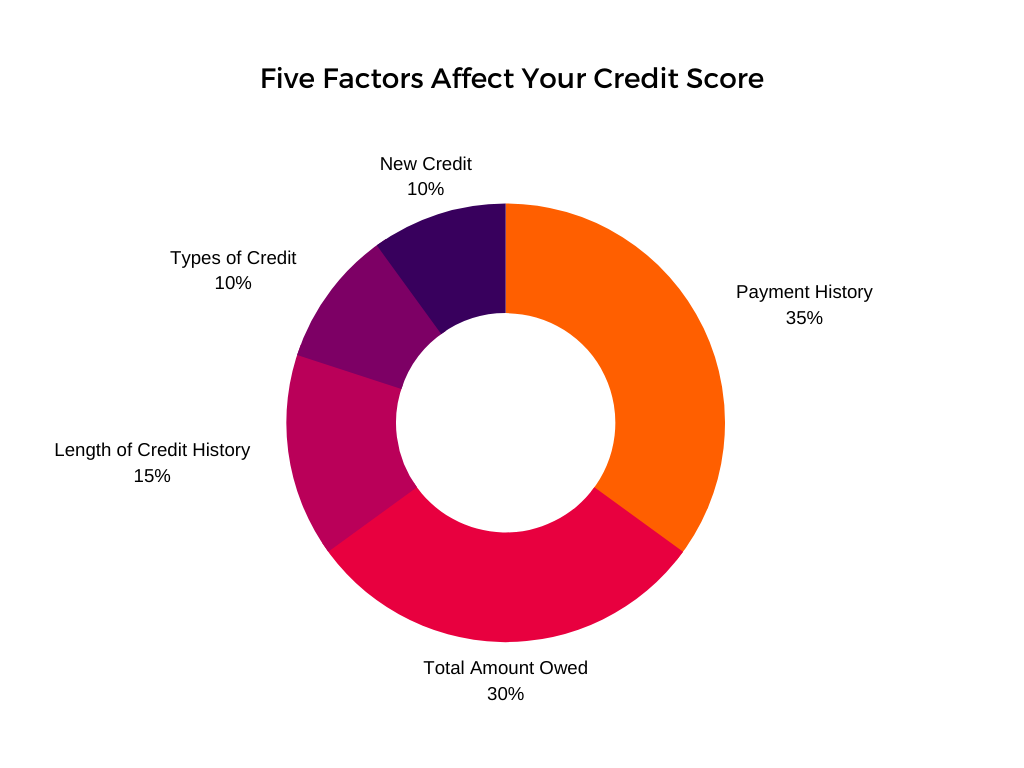

This accounts for 35% of your credit score; things like late payments on bills, repossessions, bankruptcy, and liens can cause your score to drop.

This is your debt to credit ratio and accounts for 30% of your credit score (how much debt creditors have extended to you vs. how much of the credit you’ve used).

This makes up 15% of your credit score; takes into account the average age of the accounts on your report and the age of the oldest account (in this case the older, the better).

Your "types of credit" is mix of accounts you have such as revolving debt (credit cards) and installment debt (loans); this is 10% of your credit score.

Your pursuit of new credit makes up 10% of your credit score; however, it only accounts for hard inquiries. Soft inquiries do not show up on your credit report.

[INSERT WEBINAR CTA]

To make sure your credit score stays solid, take a look at our list of credit dos & don’ts.

There are many things you can do to keep your credit score healthy. But, if your credit score is in need of repair, it may just take time to improve . The longer it has been since you have paid back a debt, the better your score is going to get. If time is of the essence, consider getting a guarantor or a cosigner on your loan.

Typically, banks require a minimum score of 680 to qualify for an SBA loan. If you don’t meet this criteria, you should consider other funding options including 401(k) business funding. Our trusted funding consultants can talk with you to determine the best funding solution for you. Connect with us today!

{kind=link}